Yesterday market was brought up by China but the global up trend ended when it reached USA. So today KLSE is most likely to open high close low.

However, there is a 30% chance KLSE can have a break from global trend today and trend higher anyhow.

If you think a tip is interesting, then most probably it will be useful to you.If you think its a lousy tip, then most probably it will bring you nothing.

Thank you to those who have taken above offers, surprisingly quite a few buyers actually didn't even realize the existence of malpf blog at all. Seems like the 'cheap' price is more an attractive point than the review writen here.

"Risk comes from not knowing what you're doing." ~ Warren Buffett"Volatility is NOT Risk." ~ David Dreman

"If you risk nothing, then you risk everything." ~ Geena Davis

For the first time in Malaysia, AmInvestment Bank Zero Strikes on Berkshire Hathaway allow investors to gain exposure to Warren Buffett’s Berkshire Hathaway Inc. Class B shares for as little as RM100 minimum investment. AmInvestment Bank Zero Strikes are a special kind of warrant listed on Bursa Malaysia, and give investors an alternative to investing in shares, Exchange Traded Funds (ETF) or unit trusts.

For the first time in Malaysia, AmInvestment Bank Zero Strikes on Berkshire Hathaway allow investors to gain exposure to Warren Buffett’s Berkshire Hathaway Inc. Class B shares for as little as RM100 minimum investment. AmInvestment Bank Zero Strikes are a special kind of warrant listed on Bursa Malaysia, and give investors an alternative to investing in shares, Exchange Traded Funds (ETF) or unit trusts.

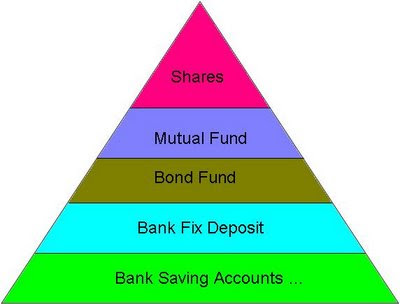

| Mutual Fund | Stocks | |

| Minimum Imposed Fee | None | $40 |

| Minimum Investment Amount | $1,000 | None |

| Investment Type | Published Fee | Put In | Get Back | Effective Rate |

| Mutual Fund | 5.5% | $1,000 | $945 | 5.5% |

| Stock | 0.7% | $5,901.30 | $5,764.98 | 2.31% |

There are a few questions why George Soros is not in my radar in this blog.

There are a few questions why George Soros is not in my radar in this blog.“Recent experience demonstrates the need for additional measures to enhance the resilience of these markets, particularly as large borrowers have experienced acute stress,” said Mr Bernanke this week.The tri-party repo market is indeed crucial but “little understood”? Perhaps only by the Fed. Witness the chairman’s comment about “experience demonstrates.”

In the context of the discussion of a crisis centered around liquidity and credit risk, the most critical thing we must know about the structure of markets is the function of the tri-party repo market.Your can read the full entries here and here.

may i ask why insurance and how insurance can really "sell"? |

everyone needs insurance, its just a matter of time when they will realize it. people who realize it earlier buy cheaper and people who realize it later buy more expensive, either way the insurance saleman earn more. ppl who never gets to realize that ended up dying with people around him realize the importance of insurance, so the next generation still buy insurance  |

I only hope that when future generations think about Bear Stearns, if they do at all, they will remember its philanthropy.This “if they do at all” is incriminating. It speaks of a self-doubt that no one reaching vice-chairmanship of a place like Bear Stearns could possibly afford to possess; the swagger of these guys was something to behold. The expression, rather, is from T. S. Eliot:

Those who have crossedMaybe I am over-interpreting, but I think in reaching to T.S. Eliot whom he must have remembered from college years, the ex vice-chairman of Bear was admitting to himself and to those who could decode him that he had been a hollow man all along.

With direct eyes, to death’s other Kingdom

Remember us – if at all – not as lost

Violent souls, but only

As the hollow men

The stuffed men.

| Khalid | RM 47,222 |

| Teresa | RM 32,830.67 |

| Yong | RM 23,322.08 |

| Liu | RM 20,722.08 |

| Rodziah | RM 18,122.08 |

| Iskandar | RM 17,722.08 |

| Iskandar | RM 17,722.08 |

| Halimah | RM 17,722.08 |

| Xavier | RM 17,722.08 |

| Yaakob | RM 17,722.08 |

| Hassan | RM 17,722.08 |

| Elizabeth | RM 17,722.08 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}