I started this Blog with very fundamental talks on personal finance on lay man write up. I have to apologize if recent posts have become quite cryptic and speculative. So let’s get back to some of the unfinished fundamentals on personal finance.

First you must have an income. Income can be any form of received money including pocket money for kids, household money received from bread earner, begged etc.

No matter how you get your income, you must setup an automated system to save part of your incom; BEFORE you do anything else ! Remember you need your ASS - Automated Saving System.

No matter how you get your income, you must setup an automated system to save part of your incom; BEFORE you do anything else ! Remember you need your ASS - Automated Saving System.

In today standard, this automated saving system should give you some interest, preferably matching fix deposit rate.

No matter if your income makes you a Rich, Average or Poor person, if you don't have an ASS you may find yourself in trouble one day. Some even cost them their lives.

Once you have enough money in your ASS, ie. can substain your lifestyle for 3, 6 or 9 months. You will need to start thinking about Money Earns Money - MeM. 'Passive' is the keyword. Something that you do once now and enjoy a life long extra income in future.

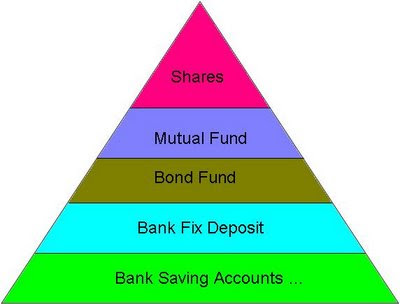

There are standard methods or PF tools to achieve MeM. Each level up the pyramid requires more learning. Entering into any of this with the wrong preception or knowledge may bring negative MeM.

There are standard methods or PF tools to achieve MeM. Each level up the pyramid requires more learning. Entering into any of this with the wrong preception or knowledge may bring negative MeM.

At this stage, many will tell you high risk high return, low risk low return. While they are not wrong, but that concept is not entirely helpful to your personal finance. In order to focus on what can helps, you may need 21st century understanding on Risk.

Further in future, you may see that MalPF will preach that

1) Personal Risk is what you know, the more you know the better it is, irrelevant to what PF tool it is

2) PF Tool Risk is fixed no matter who invest in it, irrelevan to who you are

Bundle together that 2 concepts result one simple action to position yourself well in MeM - keep learning ( the easy part ) and learn the right stuff ( the harder part - due to Rich Conspiracy ).

There are 2 BIG parts in MeM. The part mentioned above is Earn 2 with 1 or Doubling your money - MeMx2 The crucial part left out here on purpose is Time - which is also the variable for individuals.

We use Rule of 72 to quickly calculate this variable. For example, it takes 6 years to double my money if I get 12% return from my investment.

So far MalPF model works well without the need of setting goals. However MeMx2 is the part where you may see a distinctive difference between a person do it with goals and another without.

So far MalPF model works well without the need of setting goals. However MeMx2 is the part where you may see a distinctive difference between a person do it with goals and another without.Should one still find it hard to find own goals, simply follow the magic number - 7. Setup 7 MeMx2 accounts for the following:

1. Car

2. House

3. Family

4. Education

5. Retirement

6. Charity

7. Holiday and Travels

The good thing about none goal specific MeMx2 is that they are flexible and interchangable. You should start all 7 accounts at once even if you think you don't need it. Even putting in 1 cent a month into each account is better than putting 10 cent into one investment account only. ( No, this is NOT diversification, this is just broaden your availability when you don't have a target, like spreading a fish net when you don't have a hook/bait )

The second part of MeM is to Buy 100 with 1 or Secure Future Money - MeM100. Also commonly treated as insurance. While MeMx2 urges us to learn more, gain more knowledge but there are always something we haven't learned yet or will never able to 'finish' learning. Hence for all the stuff we don't know, we apply MeM100 to it.

This is especially useful when you have goals in MeMx2. For example, I want to save $100 a month for 20 years with 12% return so that I can get my $100,000 for my retirement. So I can buy a $100,000 insurance just incase if I lost my ability to save that $100, I will still get my $100,000 regardless.

This is especially useful when you have goals in MeMx2. For example, I want to save $100 a month for 20 years with 12% return so that I can get my $100,000 for my retirement. So I can buy a $100,000 insurance just incase if I lost my ability to save that $100, I will still get my $100,000 regardless.There are 5 big areas in MeM100:

1. Die Early

2. Living Dead

3. Fail to Die

4. Accident

5. Income Replacement

If you still don't have clear goals in life up to this stage. Then you will not be able to have an optimized Personal finance plan ie. Buy Term Invest The Rest. You would probably go for something traditional called Whole Life Plan. Its not bad at all for someone who cann't even figure out a single goal after 20+ years of life. Try This ...

and this is what this picture is all about ... ( may be not All but the nutshell yes )